Refinancing vs Restructuring is one of the most searched loan comparison topics among EMI calculator users, home loan borrowers, and business owners.

If you are unsure about the difference, this guide will help you understand:

-

What each term means

-

How it affects your EMI

-

Credit score impact

-

Real-life examples

-

Which option is better for your situation

Let’s break it down step by step. 👇

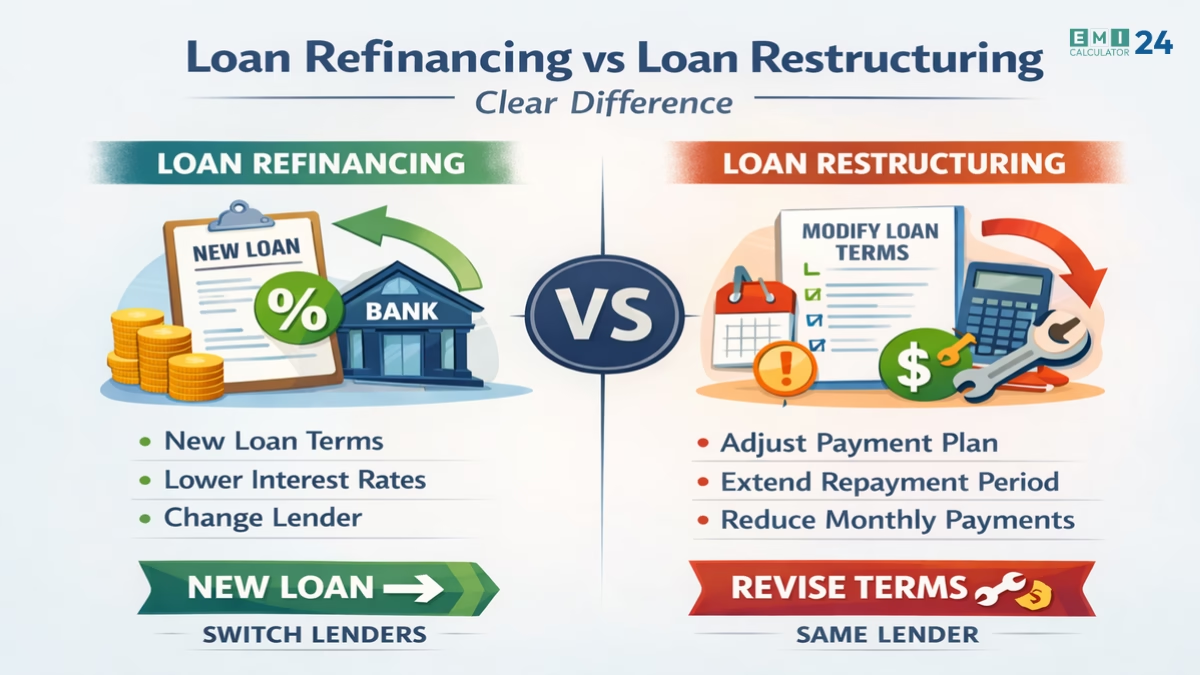

What is Loan Refinancing? 🔄

Loan refinancing means closing your old loan and taking a new loan—usually at a lower interest rate or better repayment terms.

In simple words:

-

✅ Old loan ends

-

✅ New loan starts

-

✅ Better terms apply

Why People Choose Refinancing

Common reasons borrowers refinance:

-

Lower interest rate 💸

-

Reduce EMI burden

-

Shorten loan tenure

-

Switch from floating to fixed rate

-

Move loan to another bank

Step-by-Step Refinancing Process

Check your current outstanding loan amount

Compare new interest rates

Calculate EMI after refinancing using our EMI Calculator

| Calculate EMI |

Review processing fees & hidden charges

Apply for the new loan

Old loan gets closed

Real-Life Example – Home Loan

Rahul had a ₹30 lakh home loan at 9.5% for 20 years.

After 4 years, the market rate dropped to 7.8%. He refinanced.

Result:

-

EMI reduced by ₹3,200/month

-

Total interest savings: Lakhs over tenure

-

Loan became more manageable

💡 Tip: Always check processing fees, foreclosure charges, and legal costs before refinancing.

What is Loan Restructuring? ⚡

Loan restructuring modifies your existing loan terms when you face financial hardship.

Key points:

-

No new loan

-

Same lender

-

Terms are adjusted to reduce immediate burden

When Banks Offer Restructuring

Common scenarios:

-

Job loss or salary reduction ⚠

-

Drop in business revenue

-

Medical emergency

-

Pandemic-like situations

How Loan Restructuring Works

Banks may:

-

Increase loan tenure

-

Reduce EMI temporarily

-

Offer moratoriums

-

Convert unpaid interest into principal

Real-Life Example – Salary Loss

Meena had ₹18 lakh outstanding home loan, EMI ₹22,000.

After job loss, the bank restructured her loan:

-

Tenure extended by 5 years

-

EMI reduced to ₹16,000

Takeaway: Immediate relief, but total interest increased over the loan term.

Loan Restructuring Impact on Credit Score 📉

-

May indicate financial stress

-

Future lenders may review credit history carefully

-

Not considered default but is recorded

-

Impacts your Refinancing vs Restructuring decision

Refinancing vs Restructuring Table

| Basis | Refinancing | Restructuring |

|---|---|---|

| Purpose | Save money | Financial relief |

| New Loan | Yes | No |

| Interest Rate | Usually lower | May stay same |

| EMI Impact | EMI reduces | EMI may reduce temporarily |

| Credit Score | Neutral/Positive | Possible impact |

| Best For | Stable income | Financial hardship |

EMI Impact – Refinancing vs Restructuring 💰📊

Loan Overview

| Detail | Original Loan |

|---|---|

| Loan Amount | ₹20,00,000 |

| Interest Rate | 9% |

| Tenure | 20 Years |

| EMI | ₹17,995 |

| Total Payment | ₹43,18,800 |

| Total Interest | ₹23,18,800 |

Comparison Table – Refinancing vs Restructuring

| Option | EMI | Total Payment | Total Interest | Net Impact |

|---|---|---|---|---|

| Refinancing (7.5%, 20 yrs) | ₹16,112 | ₹38,66,880 | ₹18,66,880 | Saves ₹4,51,920 |

| Restructuring (9%, 25 yrs) | ₹16,786 | ₹50,35,800 | ₹30,35,800 | Extra ₹7,17,000 |

Key Takeaways:

-

Refinancing: Lower EMI & interest → best for stable borrowers

-

Restructuring: Short-term relief, higher long-term cost → for financial stress

How to Decide Using EMI Calculator 🧮

-

Enter original loan details

-

Calculate EMI after refinancing

-

Calculate EMI after restructuring

-

Compare EMI, total interest, total repayment

💡 Tip: Don’t focus only on EMI. Consider total repayment and long-term cost.

Quick Decision Guide Table 📊

| Your Situation | Better Option |

|---|---|

| Interest rates dropped | Refinancing |

| Temporary salary loss | Restructuring |

| Strong credit score | Refinancing |

| Business slowdown | Restructuring |

| Want long-term savings | Refinancing |

Real-Life Decision Example:

-

Amit: Stable job, market rate dropped → Refinanced, saved ₹6 lakh

-

Neha: Salary cut, needed relief → Restructured, EMI reduced but tenure increased

Pros and Cons Summary

Refinancing

✅ Lower interest

✅ Reduced EMI

✅ Long-term savings

❌ Processing charges

Restructuring

✅ Temporary relief

✅ Avoid default

❌ Higher total interest

❌ Possible credit impact

FAQs

Q1: What is the difference between refinancing and restructuring loan?

A: Refinancing replaces your old loan with better terms. Restructuring modifies existing terms during hardship.

Q2: How does refinancing reduce EMI?

A: By lowering the interest rate or adjusting tenure strategically.

Q3: Does restructuring affect credit score?

A: It may indicate financial stress and impact future loan approvals, depending on reporting.

Q4: Refinancing vs restructuring – which is better?

A: Refinancing is for savings; restructuring is for temporary relief during financial difficulties.

Q5: Is refinancing a home loan to lower EMI a good idea?

A: Yes, if interest rates drop and credit score is strong.

Conclusion ✅

Refinancing vs Restructuring is not about which is universally better — it depends on your financial situation:

-

Stable income → Refinancing

-

Temporary financial hardship → Restructuring

Always calculate EMI, total interest, and repayment before deciding.

💡 Use our EMI Calculator now to make a smart, stress-free decision:

| Check Loan Eligibility | Calculate Your EMI |

Smart financial decisions today lead to a stress-free future tomorrow.