If you have ever taken a personal loan, you may have wondered how the bank decides how much interest you owe every single day. This is where Daily Interest Calculation in Personal Loan comes in. 💡 Most banks and NBFCs in India use this method to work out interest on your outstanding loan amount, and it directly affects how much you pay every month.

In this guide, we will explain everything in simple words — no confusing finance jargon, just easy examples and clear steps. Whether you are a student, a working professional, or a business owner, you will understand exactly how your loan interest is worked out. 📘

Why Understanding Daily Interest Calculation Matters

Knowing how Daily Interest Calculation in Personal Loan works helps you:

- ✅ Plan your EMI payments better

- ✅ Understand why your interest amount changes slightly every month

- ✅ Save money through smart prepayments

- ✅ Compare loan offers from different banks with confidence

Since lending practices are regulated by the Reserve Bank of India (RBI), borrowers should also review official banking guidelines before choosing a loan.

What Is Daily Interest Calculation in Personal Loan?

Meaning in Simple Words

Daily Interest Calculation in Personal Loan simply means the bank calculates interest on your loan for every single day, based on how much loan amount (principal) is still left to be paid. Instead of charging interest on the full loan amount for the whole month, the bank looks at your outstanding balance daily and adds a small interest cost for that day.

Think of it like a water tank that is slowly emptying. Every day, the bank checks how much water (loan amount) is left and charges interest only on that remaining water — not on the full tank you started with. 💧

Why Banks Use Daily Interest Calculation

Banks prefer this method because it is fair and accurate. It makes sure:

- You only pay interest on the money you still owe, not on money you have already repaid

- Your personal loan interest calculation stays connected to your actual outstanding balance

- Any early or extra payment you make immediately reduces your future interest

This method rewards borrowers who pay on time or pay a little extra whenever possible. 🙌

How Does Daily Interest Calculation Work?

Step-by-Step Process

The whole process becomes clear once you look at these steps:

- The bank notes your loan’s outstanding principal at the start of each day

- It applies your annual interest rate divided by 365 days

- This gives the interest amount for that one day

- This process repeats every day until your loan is fully paid

How Daily Balance Reduction Works

This system is officially known as the reducing balance interest method. It is called “reducing” because your loan balance keeps getting smaller every time you pay an EMI, and the interest is calculated only on this reduced amount going forward.

So, as your outstanding balance drops, your daily interest cost also drops slowly — even if your EMI amount stays the same every month. 📉

How Outstanding Balance Changes Every Day

Every EMI payment has two parts: a portion that pays off interest, and a portion that reduces your principal (main loan amount). Once your principal reduces, the next day’s interest is calculated on this smaller amount. This is the heart of Daily Interest Calculation in Personal Loan, and it repeats until the loan closes.

Personal Loan Interest Formula

Daily Interest Formula

The standard formula used for Daily Interest Calculation in Personal Loan is:

Daily Interest = (Outstanding Principal × Annual Interest Rate) ÷ 365

Formula Explained in Simple Language

This formula might look technical, but it is very simple once broken down:

- You take the loan amount that is still pending

- Multiply it by your yearly interest rate (in decimal form, like 12% = 0.12)

- Divide the result by 365, since a year has 365 days

This gives you the exact interest charged for just one day. Multiply this daily figure by the number of days in that month to get your monthly interest cost.

What Each Value Means

| Term | Meaning |

|---|---|

| Outstanding Principal | The loan amount still left to repay |

| Annual Interest Rate | The yearly interest rate set by your bank |

| 365 | Total days in a year, used to break the rate into a daily figure |

| Daily Interest | The interest charged for that specific day |

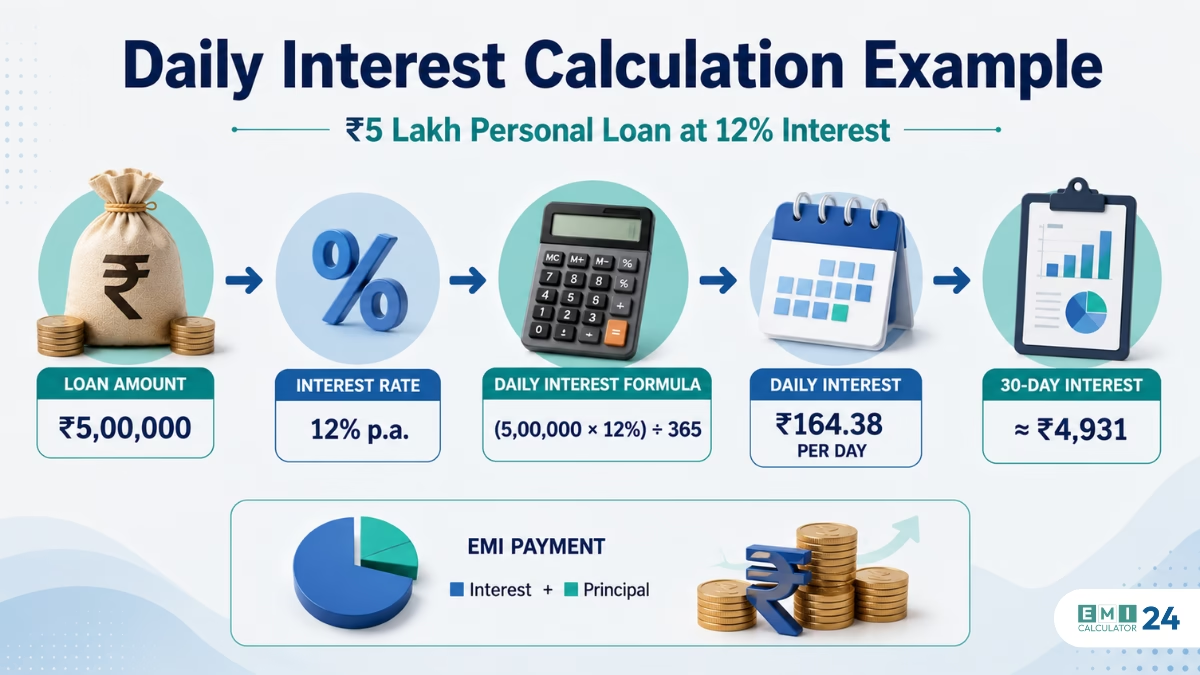

Daily Interest Calculation Example

Let’s understand this with a simple, real-life loan interest calculation example. 🧮

Example with ₹5 Lakh Personal Loan

Suppose Ravi takes a personal loan of ₹5,00,000 at an annual interest rate of 12%.

Interest Calculation for One Day

Using our formula:

Daily Interest = (₹5,00,000 × 0.12) ÷ 365 Daily Interest = ₹60,000 ÷ 365 Daily Interest = ₹164.38 (roughly)

So, on day one, Ravi is charged roughly ₹164 as interest, just for that single day.

Monthly Interest Estimate

If we assume a 30-day month and the outstanding balance stays roughly the same (before EMI reduces it), the monthly interest works out to about:

₹164.38 × 30 = ₹4,931 (approximately)

Once Ravi pays his EMI, part of it reduces the principal, so the next month’s interest amount will be slightly lower than this.

EMI Impact

This is why Daily Interest Calculation in Personal Loan directly shapes your EMI. Even though your EMI amount usually stays fixed, the interest portion inside it reduces every month, while the principal portion increases. Over time, you pay less interest and more towards clearing your actual loan. 📊

Daily Interest vs Monthly Interest Calculation

Many borrowers get confused between these two methods. Here’s a clear comparison:

| Daily Interest Calculation | Monthly Interest Calculation |

|---|---|

| Interest calculated every single day | Interest calculated once for the whole month |

| Based on the exact outstanding balance daily | Based on the balance at the start of the month |

| More accurate and fair to the borrower | Slightly less precise, may overcharge |

| Rewards early or extra payments instantly | Extra payments show benefit only next month |

| Commonly used by most Indian banks today | Used by a few older or traditional lenders |

Major Differences

The biggest difference is precision. With Daily Interest Calculation in Personal Loan, you are charged only for the exact days your money was outstanding. With monthly calculation, you might pay interest on an amount you have technically already reduced.

Which Method Is Better for Borrowers?

For most borrowers, daily calculation is more beneficial because it rewards timely and extra payments almost immediately, helping you save more in the long run. 👍

Daily Interest Calculation in Personal Loan: The Reducing Balance Approach

How It Works

This approach calculates interest fresh each day, based on your current loan balance. As explained earlier, every payment you make lowers your balance, and this lower balance becomes the base for the next day’s interest.

Why Banks Prefer It

Banks like this method because it is transparent, easy to explain to customers, and considered a fair industry standard across India’s banking and NBFC sector.

Benefits for Borrowers

- ✅ You never pay interest on an amount you’ve already repaid

- ✅ Prepayments show immediate benefit

- ✅ It encourages healthy repayment habits

- ✅ It is simple to track using an online EMI calculator

How Daily Interest Affects Your EMI

Does EMI Change Every Month?

Usually, no. Your EMI amount stays fixed for the entire loan tenure (unless you choose a floating rate loan where rates can change). However, what changes every month is how that fixed EMI is split between interest and principal.

Principal vs Interest Breakdown

Early on, most of your EMI covers interest. Over time, this flips — more goes towards your principal, less towards interest.

Interest Charged on Personal Loan Explained

This amount reduces steadily because Daily Interest Calculation in Personal Loan always works on your latest outstanding balance. This is one of the core reasons EMI interest calculation feels complex at first, but once you see it as a daily process, it becomes much easier to understand. 😊

What Happens If You Make an Early EMI Payment?

Interest Savings

If you pay your EMI a few days early, your outstanding principal reduces sooner. Since interest is calculated daily, this means fewer days of interest on the higher balance, resulting in real savings.

Effect on Outstanding Principal

Every rupee paid early directly lowers your principal faster, which means your future interest amounts also shrink faster.

Can You Reduce Total Interest?

Yes! Paying early, even by a few days each month, can add up to noticeable savings over a 3-5 year loan tenure. Small habits make a big difference over time. 💰

How Prepayment Reduces Daily Interest

Partial Prepayment

When you make a partial prepayment (paying extra money beyond your EMI), your outstanding principal drops immediately. Since Daily Interest Calculation in Personal Loan depends on this principal, your daily interest cost reduces from that point onward.

Full Prepayment

If you close your loan completely before the tenure ends, you stop paying interest altogether from that day. This is one of the biggest advantages of understanding how daily interest works.

Things to Check Before Prepaying

Before making a prepayment, always check:

- Whether your bank charges any prepayment penalty

- The minimum lock-in period before prepayment is allowed

- Whether partial or full prepayment options are available

👉 For more details, check our related article on RBI Prepayment Charges to understand your rights as a borrower.

Factors That Affect Your Daily Loan Interest

Several factors influence your Daily Interest Calculation in Personal Loan amount:

- Loan Amount – A higher loan amount means higher daily interest

- Interest Rate – A higher rate increases your daily and monthly interest cost

- Loan Tenure – Longer tenure usually means more total interest paid overall

- EMI Payment Date – Paying on or before the due date avoids extra interest days

- Outstanding Balance – A lower balance always means lower daily interest

Understanding your personal loan interest per day helps you see exactly where your money is going each month. 📅

How to Calculate Daily Interest Yourself

Manual Calculation

Doing Daily Interest Calculation in Personal Loan by hand is not difficult once you know the formula. You can calculate it manually using the formula we shared earlier:

Daily Interest = (Outstanding Principal × Annual Rate) ÷ 365

Just plug in your current loan balance and interest rate, and you’ll get your daily figure.

Calculator Method

Knowing how to calculate daily interest for personal loan manually is useful, but it can get time-consuming, especially as your balance changes every month. This is where an online personal loan interest calculator becomes handy — it does all this daily math instantly and shows you a clear month-by-month breakdown.

— Try our free EMI calculator to see your exact interest and EMI breakdown in seconds.

| Calculate Personal Loan EMI |

Simple Calculation Tips

- Always check if your interest rate is annual or monthly before calculating

- Use 365 days for annual calculations (366 in a leap year)

- Recalculate after every prepayment to see updated interest savings

Common Mistakes Borrowers Make

Avoid these common mistakes that cost borrowers extra money:

- ❌ Ignoring Daily Interest – Not realizing that even a few late days add up

- ❌ Missing EMI Due Date – This leads to extra interest days and possible penalty charges

- ❌ Paying Only Minimum Amount – This slows down principal reduction significantly

- ❌ Not Reading Loan Terms – Missing important details about prepayment or penalty charges

Tips to Reduce Interest on a Personal Loan

Here are some practical, easy-to-follow tips:

- ✅ Pay EMI on Time – Avoid any extra interest days or late fees

- ✅ Make Partial Prepayments – Whenever you have spare funds, pay extra towards your principal

- ✅ Choose Shorter Tenure – A shorter loan tenure means less total interest paid, though EMI will be higher

- ✅ Compare Interest Rates – Always compare offers from multiple banks before signing up

- ✅ Maintain Good Credit Score – A strong credit score often gets you a lower interest rate

Frequently Asked Questions (FAQs)

Q1: Is personal loan interest calculated daily?

Yes, most banks and NBFCs in India follow Daily Interest Calculation in Personal Loan, using the outstanding principal as the base for each day’s calculation.

Q2: What is the daily reducing balance method?

It is a method where interest is calculated fresh every day based on your current outstanding loan balance, rather than on the original loan amount.

Q3: Does paying EMI early reduce interest?

Yes, paying your EMI a few days early reduces the number of days interest is charged on a higher balance, which can lead to small but real savings.

Q4: Is daily interest calculation better than monthly calculation?

For most borrowers, yes. It is more accurate and rewards timely or extra payments almost immediately, unlike monthly calculation methods.

Q5: Can I calculate daily interest manually?

Yes, you can use the simple formula shared in this article. However, an online calculator makes the process much faster and more accurate.

Q6: Does prepayment reduce daily interest?

Yes, any prepayment reduces your outstanding principal instantly, which lowers the daily interest charged from that point onward.

Conclusion

Understanding Daily Interest Calculation in Personal Loan is one of the smartest things you can do as a borrower. It helps you see exactly why your EMI is split the way it is, and how small actions like early payments or prepayments can genuinely save you money. 🙂

Key Takeaways

- Each day, the bank looks at your remaining balance and adds interest on just that amount

- The formula is simple: (Principal × Rate) ÷ 365

- Prepayments and early EMI payments reduce your total interest

- Comparing rates and maintaining a good credit score both help lower costs

When Daily Interest Calculation Benefits Borrowers

This method benefits you the most when you pay on time, make occasional prepayments, and keep track of your outstanding balance regularly using a reliable EMI calculator.

Final Advice Before Taking a Personal Loan

Before signing any loan agreement, take a few minutes to do these simple checks — they can save you a lot of money later:

- ✅ Compare interest rates across at least 3-4 banks or NBFCs, not just the first offer you get

- ✅ Ask about the calculation method — confirm whether interest is charged on a daily reducing balance or monthly, since this directly affects your total cost

- ✅ Read the fine print on processing fees, prepayment charges, and foreclosure rules before you sign

- ✅ Use an online EMI calculator to test different loan amounts and tenures before finalising your decision

- ✅ Borrow only what you need — a smaller loan amount means smaller daily interest and a shorter repayment burden

Used carefully, a personal loan can support your goals instead of adding stress. The more you understand how your interest works, the more control you have over how much you actually end up paying. 🎯