Reducing balance vs daily reducing interest is a topic that many borrowers ignore while comparing loan offers. Most people focus only on the interest rate, but the way interest is calculated can significantly affect the total amount paid during the loan tenure.

A small difference in the calculation method can lead to noticeable savings over time. This becomes even more important for borrowers who make prepayments or want to close their loans early.

In this guide, we will compare reducing balance vs daily reducing interest in simple language, understand how both methods work, review examples, compare benefits and drawbacks, and see which option may help reduce the overall cost of borrowing.

What Does Interest Calculation Method Mean?

Before comparing reducing balance vs daily reducing interest, it is important to understand what an interest calculation method actually is.

Whenever a bank or lender gives a loan, interest is charged on the outstanding principal amount. However, different lenders may use different loan interest calculation methods to calculate that interest.

Why Does It Matter?

The method used can directly affect:

- Total interest paid

- Monthly repayment cost

- Loan closure speed

- Savings from prepayments

This is why borrowers should always check the interest calculation method before accepting a loan offer.

You can estimate your monthly repayments in advance with an EMI Calculator and compare different loan scenarios more accurately.

| EMI Calculator |

What Is a Reducing Balance Interest Method?

A reducing balance interest rate system calculates interest on the remaining principal amount after every EMI cycle.

As the principal decreases, the interest portion also gradually reduces.

Example:

| Particulars | Value |

|---|---|

| Loan Amount | ₹5,00,000 |

| Interest Rate | 10% |

| Tenure | 5 Years |

After each EMI payment, the outstanding balance becomes lower. The next month’s interest is calculated only on the remaining amount.

Key Features

- Widely used in India.

- Common in home loans and personal loans.

- Interest decreases as the principal decreases.

- More affordable than flat-rate interest calculations.

This method is commonly used by lenders when calculating repayments through a Home Loan EMI Calculator and Personal Loan EMI Calculator.

- Home Loan EMI Calculator

- Personal Loan EMI Calculator

| Home Loan EMI Calculator | Personal Loan EMI Calculator |

What Is Daily Reducing Interest?

Under a daily reducing interest rate system, interest is calculated every day on the outstanding loan amount.

Whenever a borrower makes a payment, the principal is adjusted immediately. Interest for the following days is calculated on the updated balance.

This method rewards borrowers who make early payments or part-prepayments during the loan tenure.

Key Benefits

- Faster reduction in interest burden.

- Better benefit from prepayments.

- More accurate interest calculation.

- Potentially lower total borrowing cost.

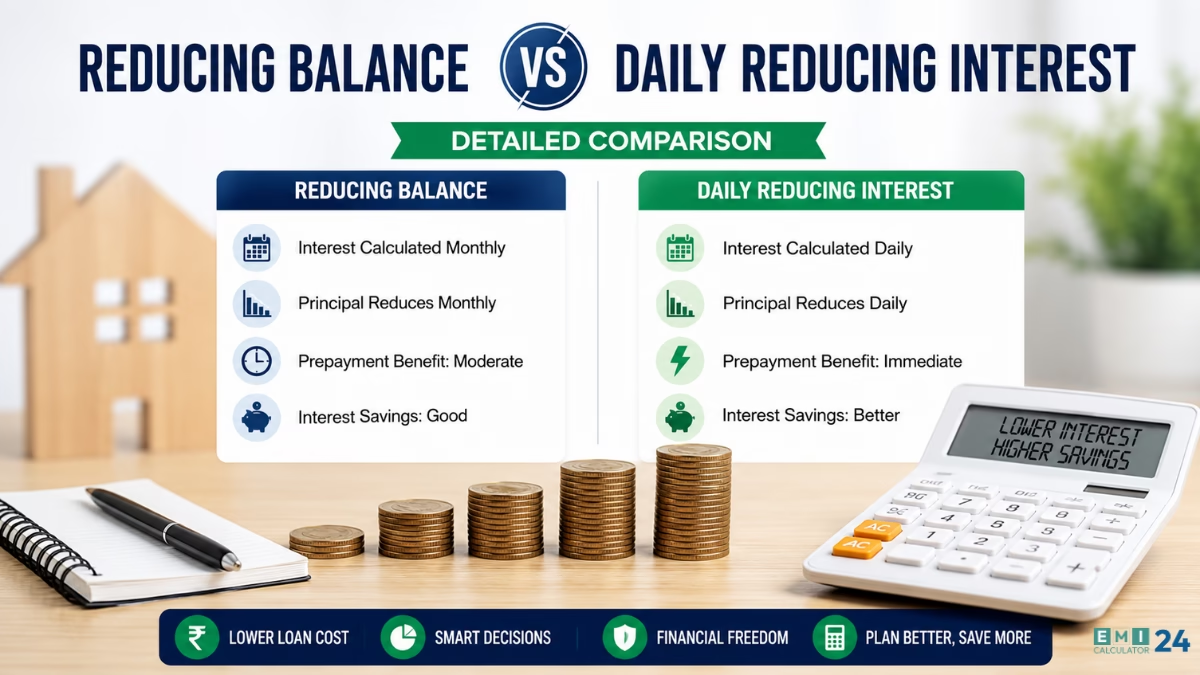

Reducing Balance vs Daily Reducing Interest – Key Differences

The biggest difference between reducing balance and daily reducing interest is the frequency at which interest is recalculated.

| Feature | Reducing Balance Method | Daily Reducing Method |

|---|---|---|

| Interest Calculation | Monthly | Daily |

| Principal Update | EMI Date | Every Day |

| Prepayment Benefit | Moderate | Immediate |

| Interest Savings | Good | Better |

| Accuracy | High | Very High |

| Loan Cost | Lower | Usually Lowest |

This comparison helps borrowers understand which loan interest method saves more money in different situations.

Example Calculation

Suppose two borrowers take a ₹10 lakh loan at 10% interest.

Borrower A

Uses reducing balance interest rate.

Makes a ₹50,000 prepayment in the middle of the month.

Borrower B

Uses daily reducing interest rate.

Makes the same ₹50,000 prepayment on the same day.

Result:

Borrower B starts saving interest immediately because the outstanding balance changes the same day.

Borrower A may receive the adjustment only in the next EMI cycle.

Over a long loan tenure, this difference can create meaningful savings.

Why Banks Use Different Loan Interest Calculation Methods

Banks choose different methods based on their lending policies and system structures.

Common reasons include:

- Product design.

- Operational convenience.

- Risk management.

- Customer segment.

Many modern lenders now prefer daily reducing interest rate calculations because they provide more transparency to borrowers.

How a Daily Reducing Interest Calculator Helps

A daily reducing interest calculator allows borrowers to estimate potential interest savings before taking a loan.

Benefits of using a daily reducing interest calculator:

- Compare loan offers.

- Understand prepayment benefits.

- Estimate future interest costs.

- Plan repayment strategies.

A daily reducing interest calculator is especially useful for borrowers planning multiple prepayments during the loan tenure.

For borrowers who want to improve their financial knowledge, the RBI Financial Education Resources also provide useful information on loans, borrowing, and personal finance.

Advantages of Daily Reducing Interest

- Better interest savings.

- Immediate benefit from prepayments.

- More accurate calculations.

- Lower overall loan cost.

- Greater repayment flexibility.

Advantages of Reducing Balance Interest

- Simple structure.

- Easy to understand.

- Commonly available.

- Suitable for standard EMI borrowers.

- Lower cost than flat interest methods.

Which Borrowers Benefit Most From Daily Reducing Interest?

The following borrowers often benefit the most:

- Salaried professionals receiving annual bonuses.

- Business owners with irregular cash inflows.

- Borrowers planning early loan closure.

- People making frequent part-payments.

For these borrowers, reducing balance vs daily reducing interest becomes an important decision factor.

Common Mistakes Borrowers Make

❌ Looking only at interest rates

❌ Ignoring calculation methods

❌ Not checking prepayment policies

❌ Comparing EMI amounts only

❌ Not using a daily reducing interest calculator before applying

Which Loan Interest Method Saves More Money?

Many borrowers ask which loan interest method saves more money.

The answer depends on repayment behaviour.

If you never make extra payments, the difference may be small.

Those who consistently make prepayments may achieve greater interest savings when their loan follows a daily reducing balance method.

This is why understanding reducing balance vs daily reducing interest is important before signing a loan agreement.

Conclusion

Choosing between reducing balance vs daily reducing interest can have a real impact on your total borrowing cost. Although both methods calculate interest on the outstanding principal, daily calculations generally provide quicker savings when extra payments are made.

Before taking any loan, compare the reducing balance interest rate and daily reducing interest rate structure carefully. Using a daily reducing interest calculator can also help estimate savings and make better borrowing decisions.

A few minutes spent understanding these loan interest calculation methods today can potentially save thousands of rupees over the life of a loan.

Frequently Asked Questions

What is the difference between reducing balance and daily reducing interest?

The main difference is calculation frequency. Reducing balance calculates interest monthly, while daily reducing interest calculates interest every day on the remaining principal.

Which loan interest method saves more money?

In many cases, daily reducing interest can save more money because extra payments reduce interest immediately.

What is a daily reducing interest calculator?

A daily reducing interest calculator is a tool that estimates loan interest based on the outstanding balance calculated every day rather than monthly.

Can prepayments reduce interest faster under daily reducing interest?

Yes. Interest starts reducing from the day the prepayment is applied to the loan account.

Is daily reducing interest better for home loans?

It can be beneficial for home loan borrowers who frequently make prepayments or additional principal payments.

Does a daily reducing interest rate lower EMIs?

Not necessarily. The EMI may remain similar, but the total interest paid during the loan tenure can be lower.